Renewables

2018 BP Energy Outlook

© BP p.l.c. 2018

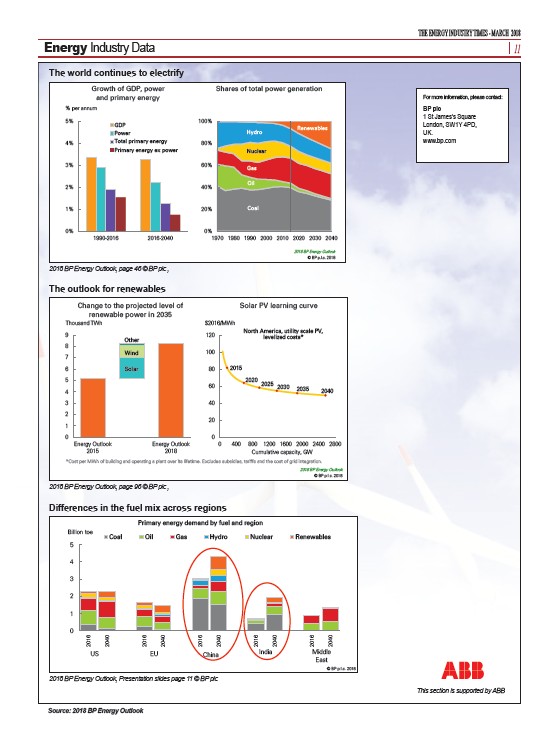

The world continues to electrify…

Growth of GDP, power

and primary energy

% per annum

Shares of total power generation

100%

80%

60%

40%

20%

0%

Hydro

Nuclear

Gas

Oil

Coal

1970 1980 1990 2000 2010 2020 2030 2040

Sectors: Power

46

5%

4%

3%

2%

1%

0%

GDP

Power

Total primary energy

Primary energy ex power

1990-2016 2016-2040

Fuels: Renewables

The outlook for renewables has increased significantly...

Solar PV learning curve

The outlook for renewables

Change to the projected level of

renewable power in 2035

Other

Wind

$2016/MWh

120

100

80

60

40

20

North America, utility scale PV,

levelized costs*

Differences in the fuel mix across regions

Coal Oil Gas Hydro Nuclear Renewables

© BP p.l.c. 2018

9

8

7

6

5

4

3

2

1

Differences in the fuel mix across regions

11

Billion toe

5

4

3

2

1

0

2016

2040

2016

2040

2016

2040

2016

2040

2016

2040

US EU China India Middle

East

Primary energy demand by fuel and region

2018 BP Energy Outlook

© BP p.l.c. 2018

0

Energy Outlook

2015

Energy Outlook

2018

Thousand TWh

Solar

0

0 400 800 1200 1600 2000 2400 2800

Cumulative capacity, GW

2015

2020

2025

2035 2040 2030

*Cost per MWh of building and operating a plant over its lifetime. Excludes subsidies, tariffs and the cost of grid integration.

96

The world continues to electrify

2018 BP Energy Outlook, page 46 © BP plc ,

2018 BP Energy Outlook, page 96 © BP plc ,

2018 BP Energy Outlook, Presentation slides page 11 © BP plc

This section is supported by ABB

Source: 2018 BP Energy Outlook

THE ENERGY INDUSTRY TIMES - MARCH 2018

Energy Industry Data 11

For more information, please contact:

BP plc

1 St James’s Square

London, SW1Y 4PD,

UK.

www.bp.com

/www.bp.com