THE ENERGY INDUSTRY TIMES - MARCH 2018

Industry Perspective 13

Towards the tipping point

If there were doubts that renewable

energy sources can compete

with oil, natural gas and coal in

power generation, developments in

the past two years should have dispelled

them. According to the International

Energy Agency (IEA), 2016

was a record year for renewable energy

projects, which provided twothirds

of new global power capacity.

This continuing growth of solar

and wind capacity in many parts of

the world, and the increasing incidence

of projects involving low or

no subsidies, have led some observers

to proclaim the arrival of a ‘tipping

point’ for renewables.

But basing this sort of assertion on

individual projects is a risky move.

After all, every project has its own

circumstances and economics, and

these can differ – sometimes considerably

– even within the same country.

Nonetheless, tipping-point predictions

do provide an indicator of

the progress made to date and what

is still required to reach the point

where renewables overtake fossil fuels

in each country’s energy balance.

This 2018 edition of the Lloyd’s

Register Technology Radar provides

an industry perspective on the challenges

that need to be overcome for

renewables to become the primary

form of energy consumed in countries.

The analysis, conducted by

Longitude in November and December

2017, is based on a Lloyd’s Register

survey of 792 executives working

in the renewable energy sector.

As a group, executives are cautious

about expectations of when renewables

will overtake fossil fuels but at

the same time are optimistic that

technology innovation in different

fields will have a sizeable impact in

the next five years on the performance

of renewable energy generation,

transmission and storage. They

also note that it is important not to

underestimate the cumulative impact

of a series of less dramatic process

improvements – especially those

powered by digital technologies.

The survey returned several key

findings. The first is that the tipping

point is still in the future. In our 2017

study, a majority of renewable sector

executives believed that parity was

being reached. This year we asked

them to predict where it would be

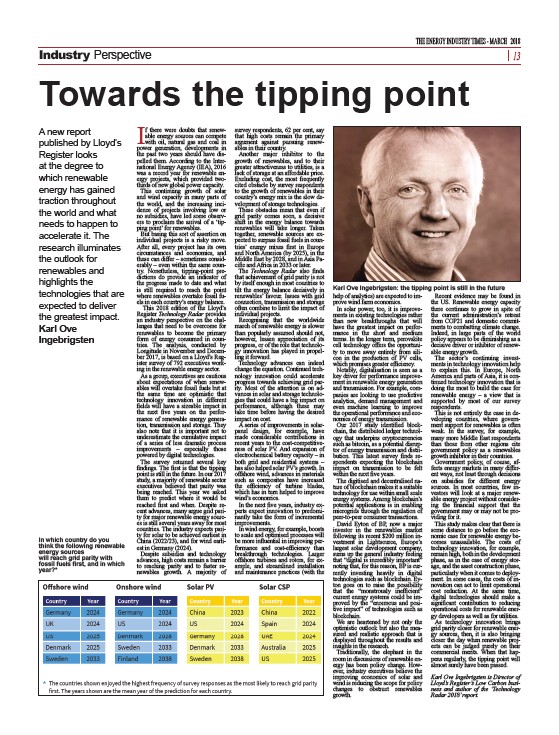

reached first and when. Despite recent

advances, many argue grid parity

for major renewable energy sources

is still several years away for most

countries. The industry expects parity

for solar to be achieved earliest in

China (2022/23), and for wind earliest

in Germany (2024).

Despite subsidies and technology

advances, high costs remain a barrier

to reaching parity and to faster renewables

growth. A majority of

survey respondents, 62 per cent, say

that high costs remain the primary

argument against pursuing renewables

in their country.

Another major inhibitor to the

growth of renewables, and to their

greater attractiveness to utilities, is a

lack of storage at an affordable price.

Excluding cost, the most frequently

cited obstacle by survey respondents

to the growth of renewables in their

country’s energy mix is the slow development

of storage technologies.

These obstacles mean that even if

grid parity comes soon, a decisive

shift in the energy balance towards

renewables will take longer. Taken

together, renewable sources are expected

to surpass fossil fuels in countries’

energy mixes first in Europe

and North America (by 2025), in the

Middle East by 2028, and in Asia Pacific

and Africa in 2033 or later.

The Technology Radar also finds

that achievement of grid parity is not

by itself enough in most countries to

tilt the energy balance decisively in

renewables’ favour. Issues with grid

connection, transmission and storage

often combine to limit the impact of

individual projects.

Recognising that the worldwide

march of renewable energy is slower

than popularly assumed should not,

however, lessen appreciation of its

progress, or of the role that technology

innovation has played in propelling

it forward.

Technology advances can indeed

change the equation. Continued technology

innovation could accelerate

progress towards achieving grid parity.

Most of the attention is on advances

in solar and storage technologies

that could have a big impact on

performance, although these may

take time before having the desired

impact on cost.

A series of improvements in solarpanel

design, for example, have

made considerable contributions in

recent years to the cost-competitiveness

of solar PV. And expansion of

electrochemical battery capacity – in

both grid and residential systems –

has also helped solar PV’s growth. In

offshore wind, advances in materials

such as composites have increased

the efficiency of turbine blades,

which has in turn helped to improve

wind’s economics.

In the next five years, industry experts

expect innovation to predominantly

take the form of incremental

improvements.

In wind energy, for example, boosts

to scale and optimised processes will

be more influential in improving performance

and cost-efficiency than

breakthrough technologies. Larger

offshore turbines and rotors, for example,

and streamlined installation

and maintenance practices (with the

help of analytics) are expected to improve

wind farm economics.

In solar power, too, it is improvements

in existing technologies rather

than new breakthroughs that will

have the greatest impact on performance

in the short and medium

terms. In the longer term, perovskite

cell technology offers the opportunity

to move away entirely from silicon

in the production of PV cells,

which promises greater efficiency.

Notably, digitalisation is seen as a

key driver for performance improvement

in renewable energy generation

and transmission. For example, companies

are looking to use predictive

analytics, demand management and

even machine learning to improve

the operational performance and economics

of energy transmission.

Our 2017 study identified blockchain,

the distributed ledger technology

that underpins cryptocurrencies

such as bitcoin, as a potential disruptor

of energy transmission and distribution.

This latest survey finds respondents

expecting the blockchain

impact on transmission to be felt

within the next five years.

The digitised and decentralised nature

of blockchain makes it a suitable

technology for use within small scale

energy systems. Among blockchain’s

potential applications is in enabling

microgrids through the regulation of

peer-to-peer consumer transactions.

David Eyton of BP, now a major

investor in the renewables market

following its recent $200 million investment

in Lightsource, Europe’s

largest solar development company,

sums up the general industry feeling

that “digital is incredibly important”

noting that, for this reason, BP is currently

investing heavily in digital

technologies such as blockchain. Eyton

goes on to raise the possibility

that the “monstrously inefficient”

current energy systems could be improved

by the “enormous and positive

impact” of technologies such as

blockchain.

We are heartened by not only the

optimistic outlook but also the measured

and realistic approach that is

displayed throughout the results and

insights in the research.

Traditionally, the elephant in the

room in discussions of renewable energy

has been policy change. However,

industry executives believe the

improving economics of solar and

wind is reducing the scope for policy

changes to obstruct renewables

growth.

Recent evidence may be found in

the US. Renewable energy capacity

there continues to grow in spite of

the current administration’s retreat

from COP21 and domestic commitments

to combatting climate change.

Indeed, in large parts of the world

policy appears to be diminishing as a

decisive driver or inhibitor of renewable

energy growth.

The sector’s continuing investments

in technology innovation help

to explain this. In Europe, North

America and parts of Asia, it is continued

technology innovation that is

doing the most to build the case for

renewable energy – a view that is

supported by most of our survey

respondents.

This is not entirely the case in developing

countries, where government

support for renewables is often

weak. In the survey, for example,

many more Middle East respondents

than those from other regions cite

government policy as a renewables

growth inhibitor in their countries.

Government policy, of course, affects

energy markets in many different

ways, not least through decisions

on subsidies for different energy

sources. In most countries, few investors

will look at a major renewable

energy project without considering

the financial support that the

government may or may not be providing

for it.

This study makes clear that there is

some distance to go before the economic

case for renewable energy becomes

unassailable. The costs of

technology innovation, for example,

remain high, both in the development

phase, as in the case of energy storage,

and the asset construction phase,

particularly when it comes to deployment.

In some cases, the costs of innovation

can act to limit operational

cost reduction. At the same time,

digital technologies should make a

significant contribution to reducing

operational costs for renewable energy

developers as well as for utilities.

As technology innovation brings

grid parity closer for renewable energy

sources, then, it is also bringing

closer the day when renewable projects

can be judged purely on their

commercial merits. When that happens

regularly, the tipping point will

almost surely have been passed.

Karl Ove Ingebrigsten is Director of

Lloyd’s Register’s Low Carbon business

and author of the ‘Technology

Radar 2018’ report.

A new report

published by Lloyd’s

Register looks

at the degree to

which renewable

energy has gained

traction throughout

the world and what

needs to happen to

accelerate it. The

research illuminates

the outlook for

renewables and

highlights the

technologies that are

expected to deliver

the greatest impact.

Karl Ove

Ingebrigsten

In which country do you

think the following renewable

energy sources

will reach grid parity with

fossil fuels first, and in which

year?*

Karl Ove Ingebrigsten: the tipping point is still in the future